Agriculture's Honest "Take 5" Weekly Roundup: 02/10/23

(~8 min read) Amazon as a wildcard, next wave of commodity demand, CEO warnings, and more...

Welcome to this week’s Agriculture’s Honest “Take 5” roundup where we break down five curated pieces of industry content. Stay tuned for this month’s deep-dive post where we evaluate a specific industry topic. Now, on to the Takes!

TAKE 1: “Amazon, an agricultural wild card”

In the Q4 2022 earnings call, Amazon discussed the decision to pause Amazon Fresh store expansions. The reasoning offered is that the combination of differentiation and economic value has not been found and until it is, the company won’t make a push here.

Following this decision, Amazon later announced a commercial deal between Amazon Fresh and Hippo Harvest, an indoor ag startup supplying leafy greens. Amazon’s interest in indoor farming isn’t new. Aside from Bezos’ personal backing of Plenty in 2017, Whole Foods has partnered with different vertical farm suppliers and the company’s Climate Pledge Fund invested in Hippo Harvest in 2021.

These actions triggered a thought-provoking question: will Amazon eventually become a farmer?

Selling commodity foods, even while branded, is a tough business to differentiate. Evidently, Amazon feels that offering fresh locally grown produce (in this case leafy greens) is a method of doing so. However, one thing that doesn’t align well with this is the often sacrifice of economic value. Indoor farming is expensive and the struggles of this have shown (particularly for vertical farms). If Amazon views this as a barrier to break, a very Amazonian method to change this would be vertical integration. From consumer goods to AWS, Amazon has been notorious for taking advantage of these market opportunities. Indoor ag, at its core, is a manufacturing and logistics business. Sure, the biological aspect makes it much more complex than consumer goods. However, Amazon is the best at solving hard problems related to this.

One huge operational challenge for indoor ag companies is offtake planning. It’s really hard to (1) find a consistent customer base to take mass volume and (2) plan offtake accurately for efficient facility utilization. Between Whole Foods and Amazon Fresh, Amazon could be highly precise in their ability to forecast demand and plan offtake accordingly. This vertical integration matched with logistical synergies would be a great start in making indoor-grown produce economical for consumers.

Andy Jassy is also very relevant to this. Before being Bezos’ successor, Jassy was the CEO of AWS for almost 20 years. He created arguably the best business unit Amazon owns today with a simple strategy:

Amazon requires vast computing power and storage to function

Other emerging internet companies need this same service

Amazon might as well vertically integrate this cost and offer it as a product

Economies of scale and trade secrete will enable Amazon to do this service better and cheaper than anyone else

Jassy is much less visionary than Bezos. His operation-first mindset has shown through cost cuts, project closures, and unwillingness to make wild bets. His bias towards tangible products makes him well-suited to cook up a vertical integration strategy of food supplies, particularly fresh produce. Not only is there better cost and control of critical supplies but it offers the chance for increased private label products, a core value creation strategy for retail and grocery. It’s a classic Jassy move.

Now, does this actually come to fruition? The probability is perhaps <25%, but that’s why it’s called a wildcard!

TAKE 2: “Agriculture’s next wave of growth”

Soybean, corn, camelina, pennycress…put them all together and what do you get…the next demand wave for row crop commodities!

For years, the industry has been consumed with the “what’s next” question in a post-ethonal world. It would appear processors, farmers, and lobbyists have found their answer in renewable diesel and aviation fuel. According to Robobank, US vegetable oil production must double by 2030 to meet the demand for renewable diesel.

")

While renewable diesel is an interesting opportunity, sustainable aviation fuel (SAF) presents the monster opportunity. As the aviation sector attempts to decarbonize, SAF made of agricultural feedstock are looked upon as the bridge from fossil fuels → electric air travel.

The International Air Transport Association (Iata) pledged in 2021 to reach net zero flying by 2050. They are relying upon a changing fuel mix to achieve two-thirds of planned GHG reductions. To put this into perspective, this means a need for 450 billion liters of sustainable aviation fuel. Today, the annual capacity is 100 million, equating to more than a 4,000x increase needed.

With all of these dynamics, everyone is trying to get a piece of it as the row crop industry looks for the next legs of structural demand. Soybean oil has driven the majority of popularity among renewable diesel with 23 new or expanded crushing plants assigned in the near term, increasing capacity by 35%. Major partnerships like ADM <> Marathon and Bunge <> Chevron have been struck as companies try to de-risk the balance of feedstock supply and commercial offtake. Other deals, particularly with corn feedstock, have included ADM <> Gevo and the recently announced Green Plains <> United Airlines for the use of sustainable aviation fuel.

Besides traditional commodity crops, other technologies are looking to make their way into the market as added options including:

CoverCress is a recently acquired startup jointly owned by Bayer, Bunge, and Chevron. The company uses a gene-edited pennywise crop that serves as an oilseed tailored for biofuel. Aside from being a cash crop, the plant also has cover crop-like characteristics boosting soil health.

Yield10 Bioscience and Mitsubishi recently signed an MOU to evaluate and establish a supply partnership for camelina, an oilseed feedstock crop catered to biofuel production. Shell and S&W also announced a camelina program via a joint venture.

While renewable diesel and sustainable aviation fuel pose structural opportunities for row crops, many claim the acre and infrastructure capacity growth required is unrealistic. However, I find these new markets to be a godsend for upholding commodity row crop demand. In a later deep-dive post, I’ll share my concern about the long-term demand for these crops and why renewable diesel and SAF are necessary for avoiding an industry-wide asset writedown.

TAKE 3: “Warnings to CEOs”

It’s no secret that the business environment for startups and technology is in a difficult place today. While rate hikes get all the blame, there’s a great deal of self-inflicted damage. Both leadership teams and venture capitalists tended to get sloppy over the past few years. A considerable part of this system slack was inaccurate forecasting. While this “J-curve” seems to be just a standard procedure of young companies, it creates second-order effects.

Irrational forecasts hurt the leadership teams as they prepare budgets and hiring plans based on these illusions. As companies made unrealistic projections over the past years, headcount grew too fast as management teams attempted to forward hire. This strategy obviously blows up if commercial traction isn’t met, leaving a substantial imbalance of headcount and product demand.

While I understand the idea of forward hiring, a better strategy should include a balance of lagging effects. If your current employees aren’t feeling a strain on their abilities, they’re likely not being pushed hard enough. Some tension and angst (at the appropriate level) are healthy for a workforce.

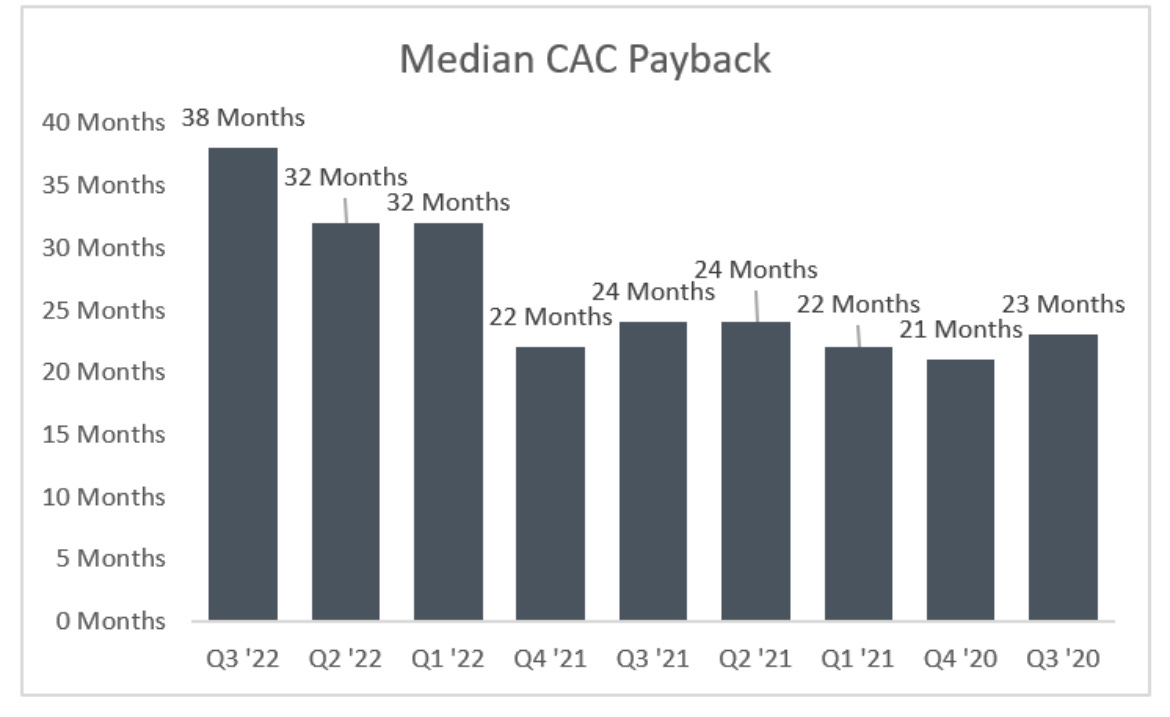

In a complementary piece related to marketing budgets, the median payback period for customer acquisition costs increased 65% during this “sloppy” era (the chart reads from right to left). Building on the prior opinion, this is just another data point that budgets were too loose with the ease of capital. Personally, I’m a fan of the zero-based budgeting methodology.

TAKE 4: “Building a toolset”

Weed resistance is a massive problem for the farmgate. A “spray and leave” strategy doesn’t work well anymore with the best available chemistries having resistance issues. Because of this, the likely path is to leverage various technologies as part of a toolset, oftentimes in an integrated pest management scheme.

Carbon Robotics offers an additional option for the toolset. The machine uses machine vision to detect weeds and kills them via high-density lasers. Aside from no mode of action that can build resistance, the unique solution is also advantaged with no root disturbance (compared to weeding) or phytotoxicity (compared to chemistry). Importantly, since this application has primary relevance to specialty crops, the 0-day preharvest interval is highly valuable in offering better harvest flexibility.

In a recent interview, the company’s founder discusses the origins of which the original intention didn’t have lasers as the answer for weed control. Through tinkering and experimentation, lasers would eventually surface as a novel solution with efficacy.

The conversation also touches on some critical KPIs including 88% effectiveness on weeds and a productivity rate of 2 acres/hr. While one would infer this is limited to smaller companies, Carbon Robotics’ average farm size is ~4k acres. For scaled operations, there’s clearly a need for numerous machines to cover material ground. At this level, the math becomes one of the unit costs and manpower to operate 2 acres/hr. If this code can be cracked (perhaps it has been), the farmer’s optionality for weed control has great value. In particular, post-emergent early-stage crops could see a redefining of crop protection tools.

TAKE 5: “Repurposing the old”

The food industry is excellent at taking products, penetrating the market with those products, and repurposing them for new growth opportunities.

The bell pepper, named by Christopher Columbus over 500 years ago, is one of these products. Snacking peppers are an up-and-coming category that markets itself on convenience and sweetness. In a world in which legacy bell peppers grow at a terminal rate, snacking peppers provides growers and CPG companies a spark of growth. The same thing happened within the snacking tomato market where repositioning a product within a legacy market turned out to be massively successful.

Aside from good marketing tactics, there’s a great effort that goes into breeding programs to deliver on this interest. Aside from snacking size, other attributes like sweetness, texture, and appearance have become major program priorities. Though not that relevant to many, it’s a fun example of how consumer trends backward integrate into legacy food creativity.

BONUS TAKE: “Super Bowl Sunday”

In light of Super Bowl LVII, I thought it would be fun to share the following fact:

The National Chicken Council (NCC) today released its annual Chicken Wing Report, projecting Americans to consume a record-breaking 1.45 billion chicken wings during Super Bowl LVII weekend. This figure represents an increase of two percent from last year’s report, the equivalent of 84 million more wings.

While I understand the flaws in this math… bear with me…

The recurring conversion seems to be ~5 wings per pound. At ~$3/Ib, this represents nearly ~$900 million in chicken wing sales for the big game!