Agriculture's Honest "Take 5" Weekly Roundup: 02/24/23

(~10 min read) Building fermentation, private label opportunities, the almond dilemma, and more...

Welcome to this week’s Agriculture’s Honest “Take 5” roundup where we break down five curated pieces of industry content. Stay tuned for this month’s deep-dive post where we evaluate a specific industry topic. Now, on to the Takes!

TAKE 1: “The battle to build fermentation”

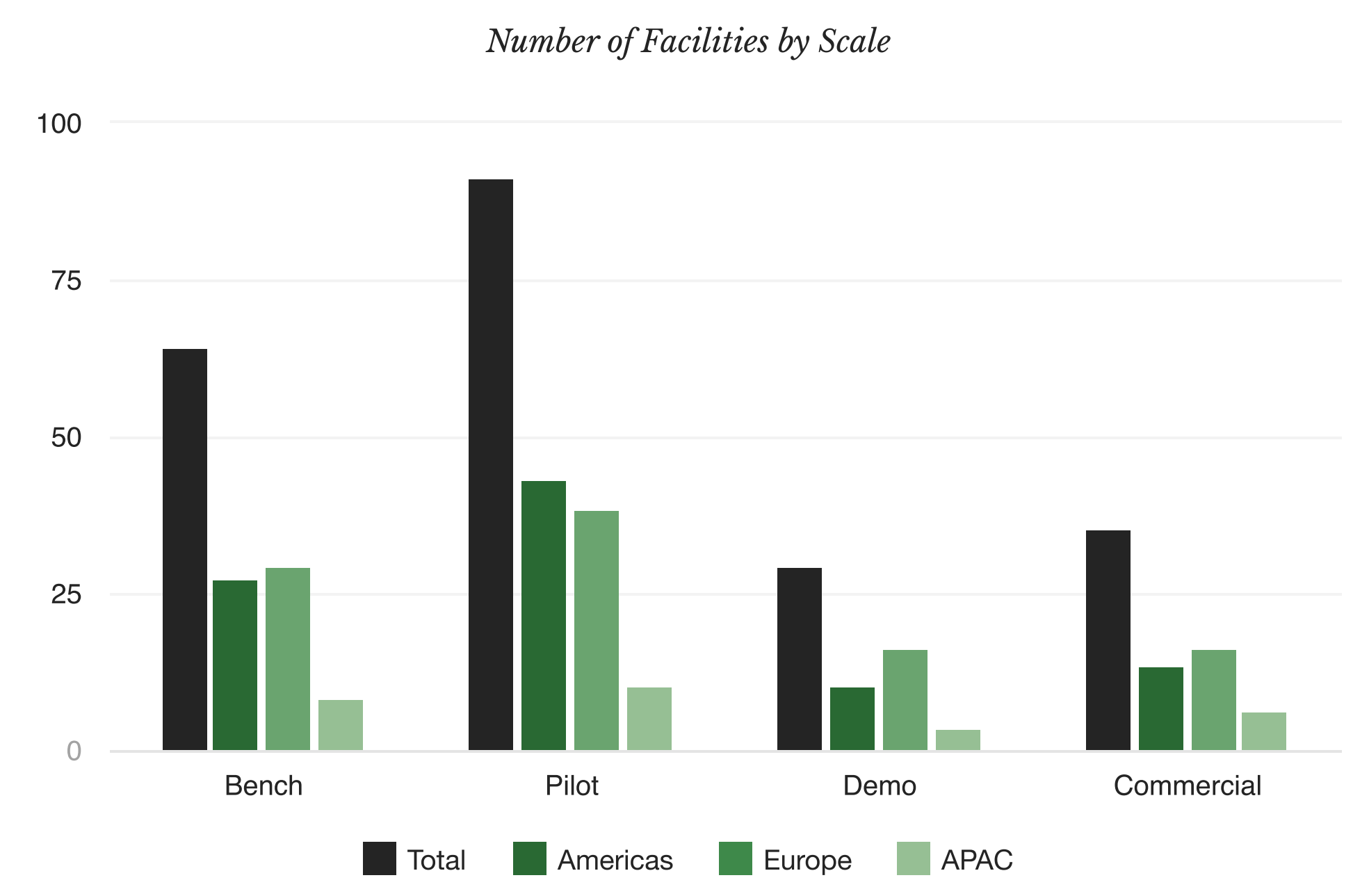

Capacitor, a fermentation database, released an insightful report on the state of global fermentation capacity. For clarity, this report isn’t near the total existing capacity worldwide. However, it’s a great sample (likely nearing 50% of current contract manufacturing capacity) that sheds light on the interests of industry participants and where a large part of infrastructure sits today.

As the report exhibits, the available infrastructure beyond the R&D and trial stages is a bottleneck. Based on Capacitor’s data, they’ve found that over 50% of users are searching for bioreactors of 20,000+ liters of capacity, though there is only ~20% of the existing facility infrastructure capable of that scale. Of the current facilities, just 16% would be considered “commercial scale” with 12% having the capacity for >500,000 liters.

The report also provides some great nuance of the systematic bioprocessing and sub-technology features that are preferred by fermentation customers.

The majority of users filtering on ‘Facility Sub-Technology’ are seeking aerobic fermentation, followed by anaerobic fermentation, spray drying and centrifugation, all of which are some of the top sub-technologies offered by the facilities on Capacitor. However, there’s a large difference in the facilities that offer aerobic fermentation (73%) and centrifugation (62%) from those that offer anaerobic fermentation (31%) and spray drying (35%), despite users showing strong interest in all of these sub-technologies.

This is an example of a holistic system requirement. Like most efforts, a silo technology or process is not that useful unless it’s incorporated within a systems approach. In this case, fermentation needs to be paired with downstream processes to provide valuable services to companies. The systems approach of an entire process brings complexity and nuance. Hence, a fermentation facility has great specialization and oversight per the industry it is catering to. It’s not that easy to retrofit an old facility to do something different or take empty capacity and get it operational in months. In fact, just 5% of contract manufacturing capacity was made for food applications.

Holding non-agriculture industries aside, the supply and demand imbalance for fermentation infrastructure and resources is an understated topic. From biological crop protection products to consumer packaged food, the entire value chain has prominent applications for fermented products. For just animal protein, it’s projected that a 100x increase in global fermentation capacity is needed by 2030 to fulfill demand.

There are some “chicken and egg” dynamics here. New commercial-scale fermentation facilities can be hundreds of millions in expenditures. To finance this, offtake agreements and customer credibility is needed. However, these customers are often VC-backed startups that may be out of money by the time the facility is built. All of this goes without saying the extreme risk that lies in scaling up from pilot/demo to bulk commercial tanks.

Most of the companies with expected demand have not proven an ability to enter the pilot/demo → commercial phase yet. For example, in looking at a leading synthetic bio manufacturer of cell-based meat, I was left quite unenthused at the likely speed and rollout of their fermentation technology. With the existing commercial square foot production and existing productivity, this current footprint could only supply 770 people if those people were to maintain per capita consumption and convert to a 100% cell-based protein diet. Another way to spin it is that every person in the US would need 226 sq feet of production space to fulfill the average diet. Hence, a 1% adoption of the US population in this specific meat would need almost 750 million sq feet of production space. Is this even realistic?

To be clear, I realize there will be major productivity improvements over the next decades. I’m highly optimistic about fermented food and ag products and believe time and scale will get us to price parities. With all the IQ and investment in this space, I’m confident there will be solutions in good time. Given the importance of the fermentation industry to future agriculture, I plan to write a deep-dive post on it in 2023.

TAKE 2: “Private label rationale”

In a great writeup of Kraft Heinz, Byrne Hobart discussed the changing dynamics of brands and in particular, private label products. He referenced how Cosco was able to position their private label brand, Kirkland, into the seventh largest CPG brand with ~$50 billion in sales. Cosco has made this possible by prioritizing quality while keeping costs low.

In ag retail, private label or proprietary products are not new. Companies like Nutrien, Wilbur-Ellis, FBN, Lavoro, and other large retailers have been leveraging this strategy for years. Nutrien, in particular, has ~2,000 proprietary products that are produced and distributed from over 30 formulation facilities. Most private label or proprietary products for these retailers have been obtained through M&A.

Hobart makes the distinction that private label brands tend to be best positioned for the middle of a price distribution curve:

As white label sales grow, stores' house brands become something more like actual brands, and tend to land squarely in the middle of the price distribution; it's hard to launch a premium specialty product, and at the low end sellers will beat one another up on gross margin for you, so the middle is where the margin is.

With respect to ag, I do believe some retailers have strong capabilities to compete in the area between private labels and premium brands.

In this area, it’s combining the aspects of quality, cost, and IP/differentiation within a private label brand. Obviously, a retailer isn’t interested in the 6-12 years of chemical or biological product development. Hence, existing products or active ingredients formulated with novelty (encapsulation, nanotech, etc.) become interesting. This solves cost structure while increasing quality and differentiated IP.

As mentioned before, this isn’t necessarily new. However, I do see expanded opportunities for this part of the market. Retailers can work with startup companies to enable this differentiated IP as a way to build a strong private label brand. Luckily for retail, a growing list of startup companies have been looking to leverage distribution channels and expertise. AgFunder’s 2022 report showed 209 financed deals in ag biotech, meaning there’s no excuse for not being able to find a startup partner to at least attempt development with. The retailer’s direct access to customers creates a strong feedback loop for the startup’s product development given this is primary market research, offering insight into what and when to develop new products. Through this kind of partnership, a retailer gets access to technology that differentiates their product and shakes the perspective that private label is of lesser quality to premium branded products, while the startup obtains an incentivized distribution channel to push a product to. It’s a great win-win made possible through the growing number of startups developing novel tech.

TAKE 3: “Our almond dilemma”

Humans love their almonds. For the middle and upper class, they’ve become a consumer staple. By 2030, another 700 million people are expected to enter “middle class” status, meaning over 50% of the global population will fall within the category. With this growth, one can assume almonds will only heighten in demand from here. There’s just one problem, California supplies ~80% of global almonds…

Despite a nearly 60% increase in acres over the past decade, prices remain quite expensive for the average consumer. Given the cost and availability concerns over water, it’s fair to say almonds won’t become cheaper. In last week’s newsletter, I highlighted the concern for California production with increased water uncertainty. This week, Stuart Woolf of Woolf Farming did a wonderful job communicating the weird dynamics of California water:

While Stuart has worked to get his water application dialed in, many farmers in California are not using any of these practices or technologies because they have reliable access to cheap water. While Stuart’s water costs $1500/acre-foot, land just 120 miles away has reliable water access at $15/acre-foot.

With hundreds of thousands of acres potentially turning to fallow in coming years, almond lovers are sure to be disappointed. With the largest global region investigating its water viability with a crop that requires as much annual water as all of California's homes, planning for a tree that takes nearly a decade to produce is very risky. Hence, increased demand + supply uncertainty → less affordable almonds. Which global regions will step up to take the load of California’s concerning situation?

TAKE 4: “A different spin on gene editing”

The communicated benefits of gene edited crops have historically been about productivity and yield improvement for farmers. This makes sense as the economic benefits must start with the farmer in mind as they need to be convinced to produce it.

In this announcement, however, the positioning was different. In Europe’s first gene edited wheat trial, researchers used CRISPR to eliminate a gene related to asparagine. When cooked, asparagine converts into acrylamide which is known as a likely carcinogen. The gene edited wheat resulted in a 45% reduction of acrylamide post-cooking. In a world where processors must monitor and regulate acrylamide, a reduction of the substance in their raw materials has great value. In a complementary article, researchers are aggressively investigating cereal grains and peanut genomes to lessen the impact on allergens and specifically celiac disease.

These applications of gene editing begin to differentiate the historical conversations and notions that governments and consumers have had toward genetic engineering techniques. Instead of just producing more quantity, the product value increases with quality. Carcinogen and allergen reductions are just some of the many applications where a plant genome can be manipulated to create a more safe and healthy product for consumers. This argument positions gene editing much differently and likely makes regulation progress much easier for strict governments like the European Union.

For the ag value chain, this also presents an example of how farmers can see better economics on quality adjustments versus yield productivity. Today, farmers do get paid on quality standards. However, they’re quite general (e.g. protein). With new crop genetic features like the GE wheat demonstrated above (low acrylamide wheat), there’s an entirely new value component unlocked. Hence, with GE crops, it’s not unrealistic to think that CPG and value chain participants will drive farmgate value more than sole yield improvements.

TAKE 5: “Delivering new products with zero marginal cost”

In a past Weekly Roundup edition, I highlighted Carbon Robotics as an additional option in the toolset to fight weed resistance. In Carbon Robotic’s case, the tool is a laser that zaps and kills weeds.

As a follow-up to “laser weeding”, Carbon Robotics recently announced new functionality for “laser thinning”. In certain crops, it’s common to overseed in order to receive optimal germination. However, this can also lead to an oversupply of plants competing with each other. Thinning is used to clean up and eliminate a percentage of plants so that the production phase of vegetative fruiting and yield can be optimized.

This product release emphasizes a critical feature of software-enabled hardware. With just a software update, Carbon Robotics was able to add this entirely new product to each existing unit without selling new equipment. No customer acquisition or infrastructure costs are required.

This is an example of how recurring revenue subscriptions can be justified. Too often I see companies wanting to start or pivot to subscription-based businesses without the means to support this business model. Providing a reason to have your customers continuously pay a recurring expense is central to making “as-a-service” models work. Historically, farmers (and the industry at large) have not been accustomed to this sales model. Hence, there’s immediate skepticism about paying a vendor every month or year for a service.

For the technology provider, it’s critical to communicate the benefits a customer will see by subscribing to a recurring expense. For many companies, it’s new products and increased reliability/efficacy of the existing product. If companies can successfully do this, there’s a clear path for recurring revenue business models in ag, particularly with intelligently automated equipment.