Agriculture's Honest "Take 5" Weekly Roundup: 02/03/23

Agriculture's Honest "Take 5" Weekly Roundup: 02/03/23

(~6 min read) CEA closures, segmentation, FMS reflections, and more...

Welcome to this week’s Agriculture’s Honest “Take 5” roundup where we break down five curated pieces of industry content. Stay tuned for this month’s deep-dive post where we evaluate a specific industry topic. Now, on to the Takes!

TAKE 1: “Reining in controlled environment ag expansions”

Plenty is the latest controlled-environment agriculture startup to announce a cutback in operations. Call me crazy, but 2022 and 2023 are not prime years to have large multi-million dollar capital projects with operations highly reliant on energy and labor as top inputs. With projects of this complexity, there are 12-24+ months in upstart time, meaning there’s a lagging effect that occurs in resulting carnage. Since 2020, $3 billion in funding has gone towards indoor agriculture with more than 90% of capital going towards the vertical farm and greenhouse operations (not “picks and shovels” technology). Given the capital outlay timing, it’s likely that many of these projects will see mid-year halts or complete shutdowns. Plenty’s September 2022 announcement of a Virginia farm expansion had broken ground with the first crop available in winter 2023/2024. With the San Fransico facilities closure, it’s hard to imagine run-rate expansion growth continues as planned. The spiraling effect for many of these CEA growers will be delayed projects → delayed revenue → increased burn and time to market → lack of investor interest…not a great equation!

Like many tech companies who overhired in a hot market cycle, CEA companies grew infrastructure projects too quickly. With a low cost of capital, budget overruns and additional buildouts were less of an issue. However, it’s now the complete opposite. For many indoor ag companies, 2023 will be a year of restructuring and focusing on existing operations that can be turned profitable. Like most things with enough time, exuberance will breed discipline.

TAKE 2: “Segmentation”

Despite seeing a 90% stock collapse from the SPAC, Local Bounti’s production process is one to watch in controlled environment agriculture. The company’s philosophy is unique in the sense that they are less worried about “technology made here” and would rather prioritize available technologies that enable the best productivity for their operation (though there’s a little irony in their patented “Stack and Flow Technology”).

It’s common for early players of category creation, CEA in this respect, to attempt everything themselves. Many CEA growers take on entire value chain risk by developing proprietary tech (hardware + software), growing the crop, and creating the brand. A model where one develops all their own tech that’s limited to only your operation to produce a commodity will be hard to earn a good return on invested capital.

In light of the model’s shortfalls, Local Bounti has prompted a move to source readily available technology that best supports unit economics. It seems like this is a trend that’s now materializing as CEA operations realize it’s not in their best interest to do everything internally. Ultimately, the segmentation of different products and services will be good for the maturity of the CEA industry.

TAKE 3: “Farm management software reflections”

It’s no secret that the category of farm management software has burned through significant investment with little industry-wide traction to show for it. Janette Barnard doesn’t hold back in her blunt perspective of the FMS wash. After $400 million of invested capital, the category has struggled to earn a profit on those technologies sustainably.

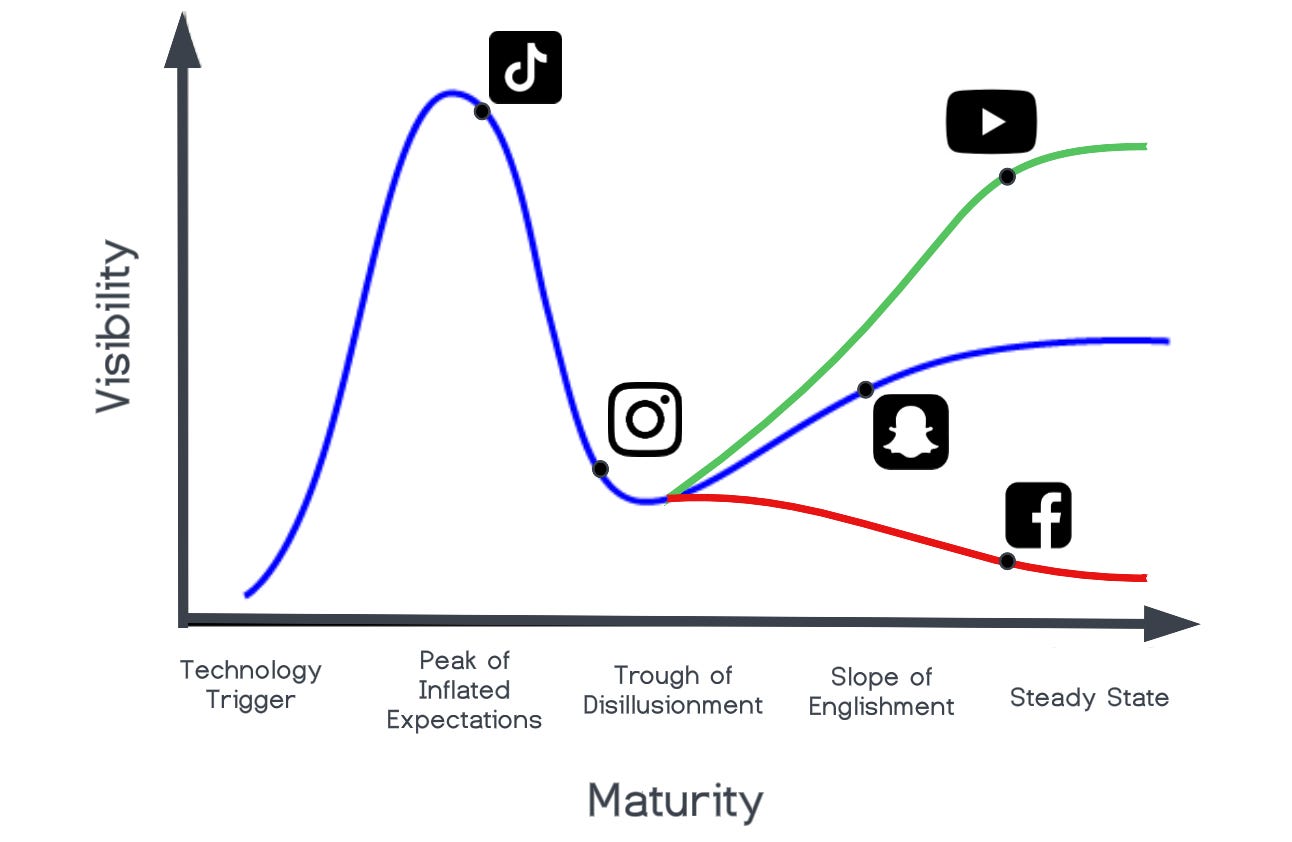

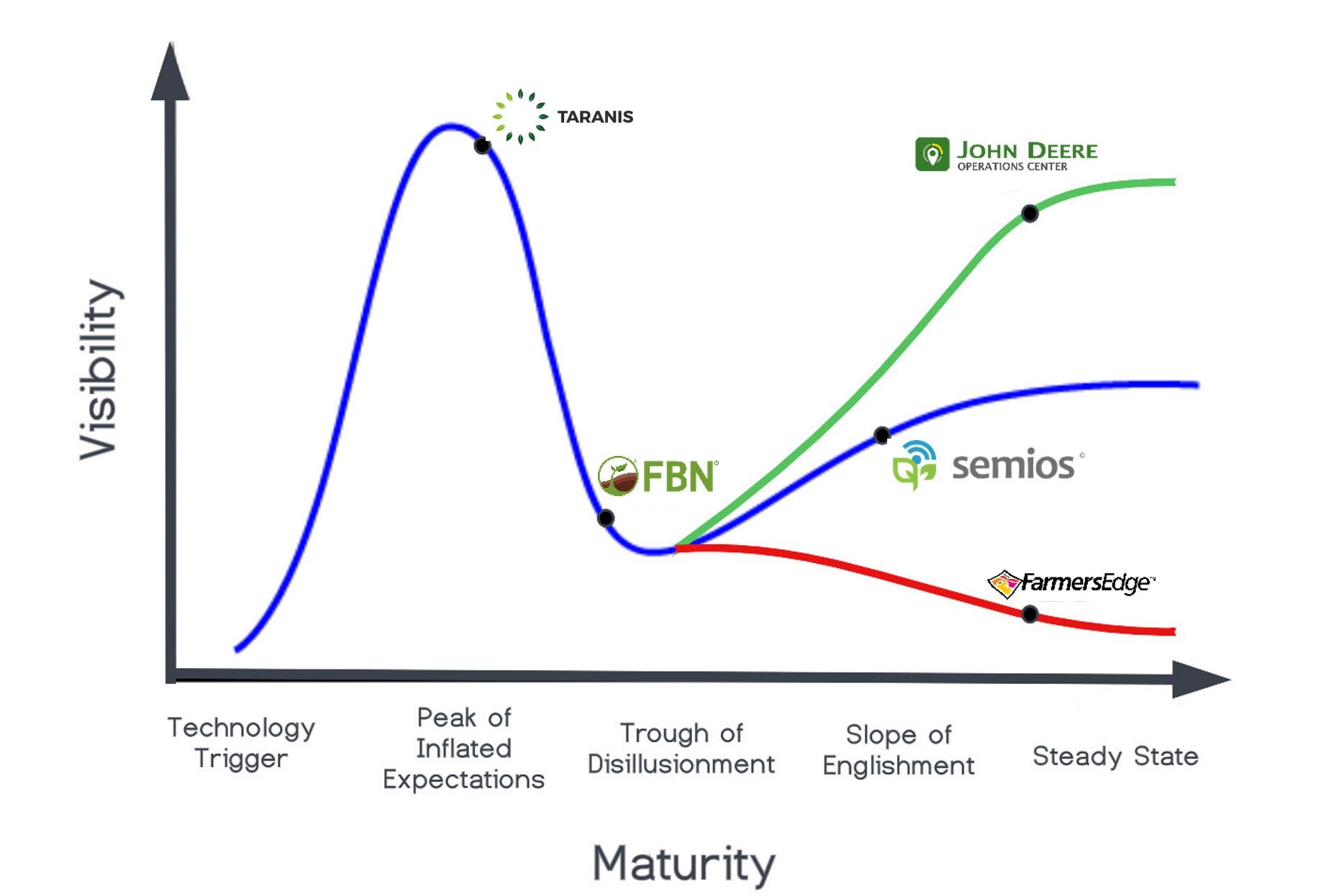

The Accelerated newsletter recently had an interesting chart plotting the hype curve for the most relevant social media companies. With enough time under our belt, we can really see where sustaining momentum presents itself.

In light of this chart, I wanted to do something similar for agtech analytics which has a similar founding timeline as the social media category. For companies at peak and trough, the story is still unwritten. However, as time makes its way through the slope of enlightenment, the commercial viability becomes clear.

TAKE 4: “Technology complements”

While integrated pest management systems have been around for 70+ years, the effectiveness is really only meeting fruition now given the continued advancements of biological controls. This week, Bayer announced a distribution deal with M2i for the delivery of pheromones in distinct specialty crops. Mating disruption, through the use of pheromones, can be used in an IPM program with chemistry applications as a natural way to suppress the pest population and lower the frequency of chemical spray applications.

As the announcement also notes, there will be the deployment of pest detection technology to serve as a precision tool for more efficient pheromone use. Under this scenario, pest detection analytics serve as a complement to pheromones. Complementary products mutually rise in popularity. Another relationship between complementary products is that lowing the price for one can increase the value of the other. For example, if Las Vegas flight fares are low, it increases the value of the casinos as there will be increased demand. Joe Spolsky makes a great point that smart companies try to commoditize their products’ complements. For agrochemical companies, pest analytics can create precision-tailored prescriptions based on pest pressure and time. In other words, pest analytics has the ability to increase the value of crop protection products. Therefore, it would be in an agrochemical company’s best interest to commoditize the service of pest analytics.

TAKE 5: “Concentrated customers”

This press release is about a greenhouse acquisition but the actual transaction has nothing to do with my interest. The article reads:

Canada boasts one of the most robust greenhouse produce sectors in the world. Ontario alone has one of the highest concentrations of greenhouse facilities and ag-tech professional talent. This region consists of over 200 greenhouse farms growing a variety of produce on over 3,000 acres. These high-tech growing methods can yield up to 20 times more product per acre and utilize less water and less input than traditional farming methods. Every year, Ontario greenhouse farms grow in excess of 520,000 tons of produce and are leading the world in resilient and sustainable vegetable production.

A problem that software has created for VC-backed bio and hardware startups is the illusion of scale. Software products have the exact marginal cost whether it’s a prospective customer 1 mile or 1,000 miles away from headquarters. For hardware or physically-enabled products, it’s different.

Many robotic agtech companies are attempting to deploy robots-as-a-service (RaaS) business models. For resource-strapped startups, it’s difficult deploying robots across broad geographical markets. Aside from assembly, the servicing needs can quickly become out of hand. For this reason, it’s critical for robotic companies to carefully know their market and where the highest customer concentration lies. Luckily, ag production tends to be highly concentrated in specific areas due to inherent climate factors (wine grapes in CA, apples in WA, vine crops in Ontario, etc.). For startups, instead of giving off an illusion of growth based on geography, it’s more critical to dominate a concentrated market and build from there.